Flat vs Reducing Interest: The Hidden Truth

Don't fall for low flat rates. Learn how reducing balance interest works and why it's almost always the cheaper option for your loan.

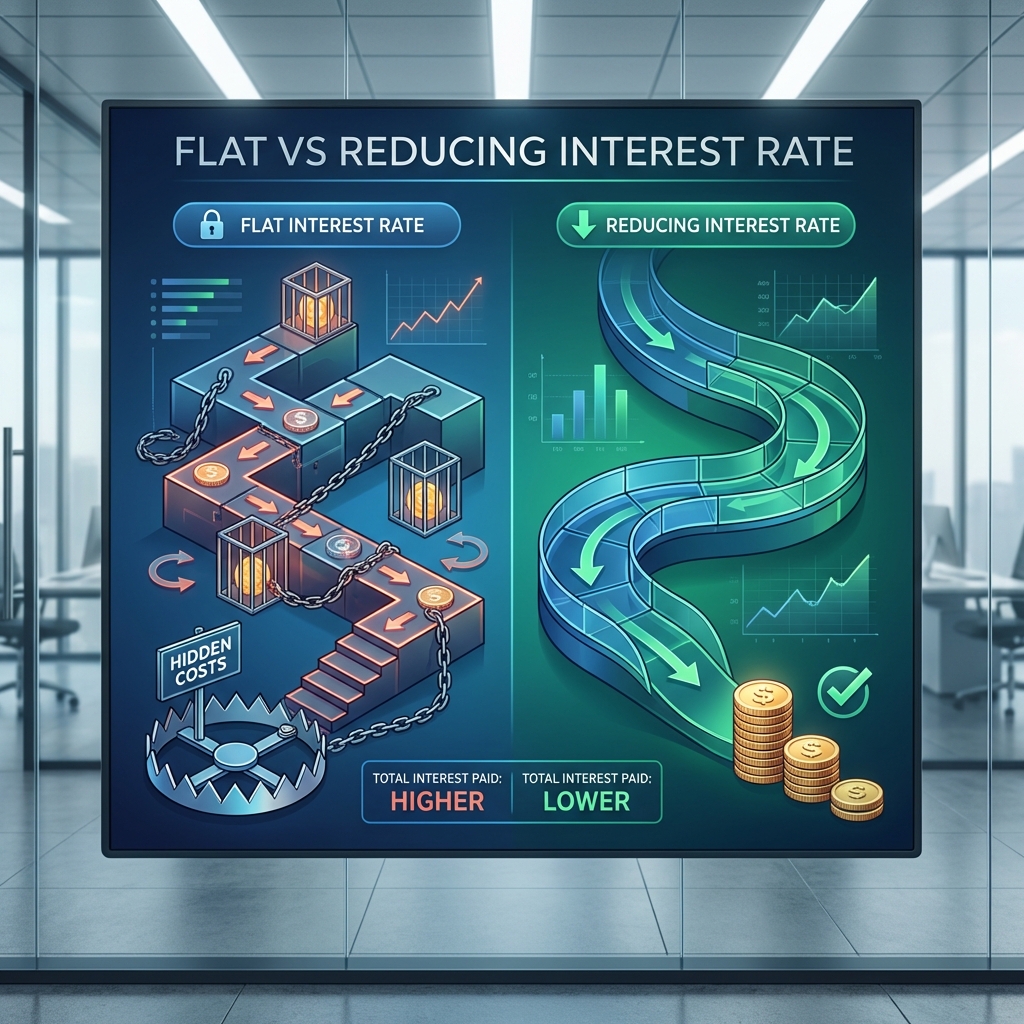

A "Fixed Rate" of 10% sounds better than a "Reducing Rate" of 15%, right? Wrong. In the world of loans, the way interest is calculated is more important than the percentage itself.

The Flat Rate Trap

In a Flat Rate Loan, interest is calculated on the full principal amount throughout the entire tenure. Even after you've paid back 90% of your loan, you're still paying interest on the 100% you originally borrowed. This is why flat rates are often used in "too good to be true" personal or car loan offers.

The Reducing Balance Advantage

A Reducing Balance Rate calculates interest only on the outstanding principal. As you pay your EMIs, your principal decreases, and so does the interest you owe. Over a 5-year tenure, a 10% Flat rate is roughly equivalent to an 18%+ Reducing rate!

The Real Math

Flat Rate (10%)

₹1,50,000 Total Interest

On a 5 Lakh loan for 3 years

Reducing Rate (10%)

₹81,232 Total Interest

On same loan. You save ₹68,768!

"Always ask for the 'Effective IRR' or the reducing balance equivalent before signing any loan document."